DolphinDB-Powered FICC Brain: Real-Time Insight, Smarter Returns, Stronger Defense

In investment management, precision and transparency are now essential for institutional competitiveness. Facing challenges from massive heterogeneous data, complex P&L calculations, and real-time risk control, DolphinDB partnered with a leading securities firm to build a next-generation FICC intelligent risk and performance platform.

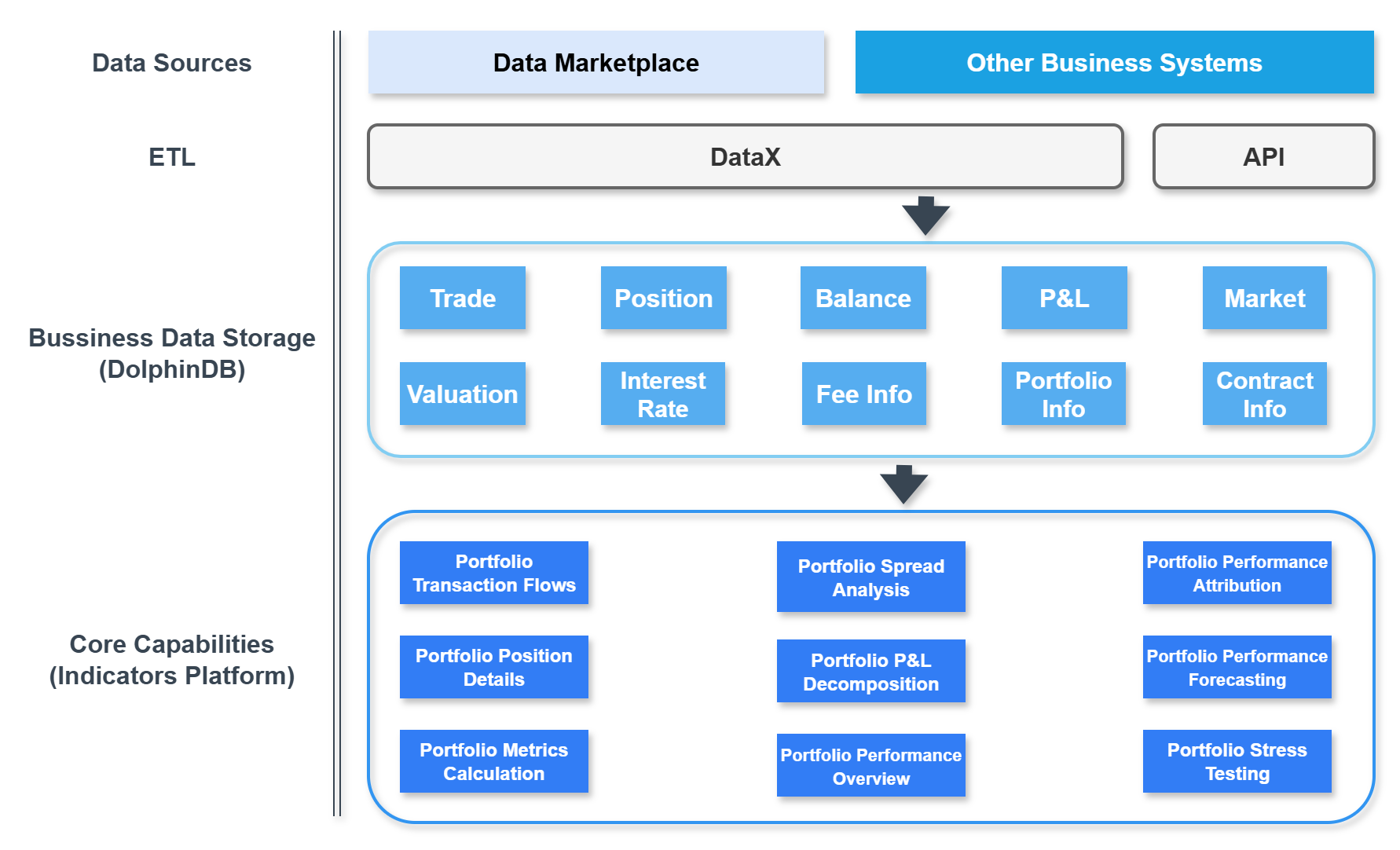

The system features a three-tier architecture: "real-time insights – attribution analysis – risk forecasting." It modernizes the quantitative infrastructure for fixed-income asset management and delivers data-driven intelligence for investment decisions.

The Challenge: Managing Trillion-Scale FICC Data

As a leading securities firm managing ten major asset categories—including bonds, convertible bonds, futures, and options—the institution faces significant data complexity. The FICC business handles over 100 original data tables, with transaction records in the millions and position/balance tables exceeding hundreds of millions of entries. With trillion-scale historical data across highly heterogeneous asset classes, the firm must navigate complex P&L calculations and analytics spanning more than ten key metrics including cost basis, market value, and interest income.

As business scope and data volumes expanded, the legacy risk and performance system revealed critical limitations:

- Performance Bottlenecks: Covering 20+ markets and 100,000+ securities, the system relies on overnight batch processing for risk indicators. Processing trillion-scale historical pricing data takes hours, missing critical timeliness requirements.

- Slow New Product Onboarding: Adding new asset types requires vendor-led custom development, with cycles often exceeding two weeks. Each derivative product demands rebuilding entire data pipelines, delaying time-to-market.

- High Operational Overhead: The Oracle + Java architecture lacks business-friendly middleware. Supporting two separate technology stacks requires multiple IT teams, inflating development and maintenance costs.

- Opaque "Black-Box" Operations: The vendor-built Oracle + Java system contains complex, proprietary code logic. Calculation discrepancies arise with no clear path to diagnosis or resolution.

The DolphinDB Solution

To address these challenges, DolphinDB partnered with the securities firm to build an integrated fixed-income intelligence platform centered on "insight–attribution–forecast" capabilities. Built on DolphinDB's high-performance time-series database, the system strengthens core portfolio management through granular position monitoring, rigorous performance decomposition, and forward-looking stress testing—providing a robust data foundation for investment decisions.

Real-Time Portfolio Visibility

The platform tracks transaction flows, analyzes detailed holdings, and dynamically calculates key metrics to enable second-level monitoring of trillion-scale portfolios. Portfolio managers gain continuous visibility into risk exposures and asset allocations, eliminating traditional manual reporting delays.

Granular P &L Attribution

Using the Campisi decomposition model, the system breaks down returns into fundamental components—coupon income, spread income, and capital gains. Multi-dimensional attribution analysis pinpoints the precise drivers of alpha generation (such as duration positioning), enabling continuous strategy refinement.

Proactive Defense Against Extreme Risk

Through interest rate scenario simulations and historical stress tests (including 2008 financial crisis conditions and liquidity shocks), the system quantifies portfolio behavior under extreme market conditions. This forward-looking approach transforms risk management from reactive post-mortem analysis to proactive defense.

DolphinDB's Technical Advantages

Handling hundreds of millions of position records, millions of trades, and complex multi-table joins, the platform leverages DolphinDB's computational performance to ensure efficient execution of critical queries and P&L calculations:

- Efficient Data Storage: Hybrid partitioning combined with columnar time-series storage and ZSTD compression reduces historical data storage costs by approximately 70%. Multi-hundred-million record joins return results in seconds, optimizing hardware utilization while accommodating the firm's massive, heterogeneous datasets.

- Rapid Development: DolphinDB's SQL-like scripting language lowers development barriers significantly. With 2,000+ built-in functions, 10+ streaming engines, and comprehensive business components, it provides end-to-end analytics capabilities. A single SQL statement can seamlessly join real-time streams with 10 years of historical data, supporting backtesting across equities, futures, options, bonds, and margin trading.

- Reduced IT Overhead: The unified storage-compute architecture simplifies system design and dramatically cuts development and maintenance costs. Transparent, traceable business logic eliminates "black-box" risks. Trading teams can conduct independent data analysis, reducing IT dependencies and improving operational efficiency.

- Real-Time Risk Monitoring: For FICC trading, DolphinDB calculates risk metrics—including VaR, credit spreads, and duration measures—in real time. Combined with intuitive visualization and automated alerting, this enables trading teams to adjust strategies promptly and maintain continuous risk control.

The Gains

DolphinDB's customized intelligent FICC platform delivered substantial improvements in both performance and cost efficiency for the securities firm.

Performance Enhancement & Cost Optimization

Data query latency dropped from minutes to seconds, with real-time computation response speed increasing 10x across key metrics. Script-based development reduced code volume by 70%, with function library reusability exceeding 90%. Development cycles shortened to weekly iterations. Columnar storage and in-memory computing improved hardware utilization by over 60%, reducing server footprint by 50% for equivalent data volumes.

Business Value

- Real-Time Risk Defense: Second-level portfolio exposure monitoring provides transparent, traceable visibility into positions, P&L, and risk metrics in real time.

- Intelligent Performance Attribution: Comprehensive P&L decomposition calculations accelerated 100x, enabling precise analysis of bond portfolio return drivers.

- Proactive Risk Management: Historical scenario-based stress testing and quantitative extreme loss estimation capabilities upgraded the firm's forward-looking risk control framework.