Case Study | Factor Development Reimagined: What's Powering Top Hedge Funds

The financial industry is experiencing a fundamental shift in how factor development works. Quantitative trading and AI-driven research are no longer content with T+1 analysis — waiting until the market closes to crunch the numbers. The new standard? Real-time, millisecond-level responses.

This shift demands a level of speed, consistency, and efficiency that traditional factor development platforms simply weren’t built for.

Recognizing this challenge, several leading hedge funds turned to DolphinDB to build next-generationfactor development platforms with unified batch and stream processing. The results:

- 10× faster end-to-end workflows

- Factor calculations in milliseconds , not minutes

- Historical backtests 100× faster

These gains go beyond raw performance — they represent a decisive step toward truly real-time, intelligent quantitative research.

The Challenge: When Milliseconds Make Millions

Modern quant trading operates in a world where speed isn't just an advantage — it's survival. High-frequency trading demands factor calculations that finish in under 10ms, while the entire journey from signal generation to order execution must happen within 50ms. Strategy development cycles have compressed from months to weeks or even days.

Meanwhile, the data explosion continues. Hedge funds now trade across stocks, futures, options, and alternative assets, processing hundreds of data dimensions — from traditional price-volume metrics to satellite imagery and social sentiment. Terabytes flow in daily, creating unprecedented computational demands.

The old way of doing things simply doesn't work anymore. The question facing every quantitative fund is clear: how do you build a platform that can handle today's data volumes while delivering the speed and reliability that modern markets demand?

Breaking Points: Where Traditional Architectures Hit the Wall

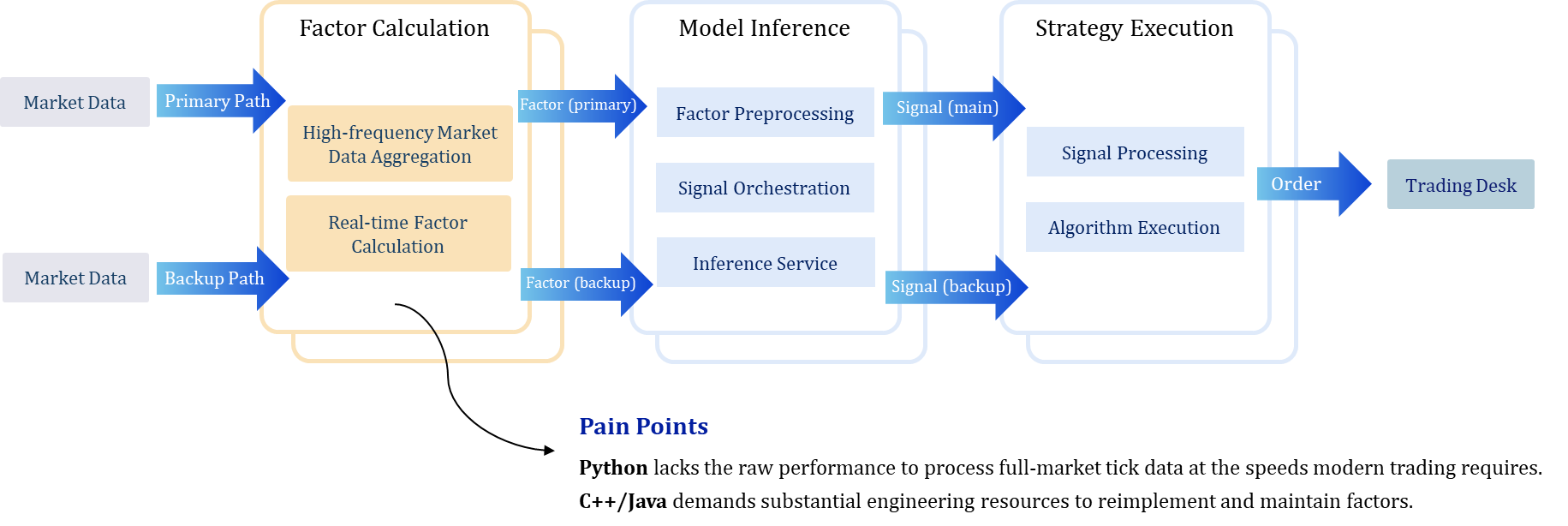

Here’s a typical live trading workflow:

In such workflows, traditional factor development platforms suffer from:

Fragmented Development Creates Risky Gaps

The typical workflow splits research and production into separate worlds. Teams develop factors in Python for research, then completely reimplement them in Java or C++ for production deployment. This code migration process is painfully slow, inherently error-prone, and introduces significant risk. When backtest results don't match live performance due to implementation differences, entire strategies can fail in real markets.

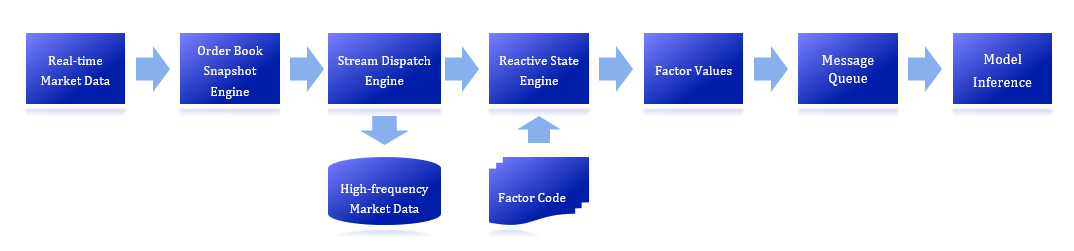

Real-Time Performance Falls Short of Market Demands

Traditional streaming platforms like Flink struggle to meet HFT requirements, often delivering factor calculations with over 100ms latency — far beyond the 10ms threshold needed for competitive trading. The problem compounds with complex factors like order book liquidity metrics, where latency grows exponentially as data complexity increases, making sophisticated strategies practically unusable in real-time.

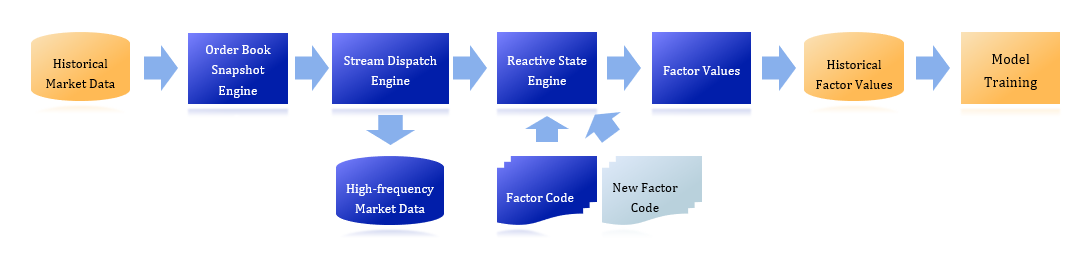

Historical Backtesting Becomes a Bottleneck

Simple backtests have become multi-hour ordeals. Testing a single factor across the entire market routinely takes eight hours or more. When teams attempt multi-factor parallel testing to accelerate development cycles, resource consumption explodes, driving up infrastructure costs while still delivering frustratingly slow iteration speeds.

Technology Stack Complexity Drains Resources

Modern factor platforms cobble together multiple languages (Python, Java, C++) with separate environments for each stage — Jupyter for research, Flink for production streaming. Data gets scattered across HDFS, MySQL, Redis, and other systems, creating a maintenance nightmare that consumes engineering resources that should be focused on strategy development rather than infrastructure management.

Therefore, hedge funds require a next-generation factor development platform that breaks through the limitations of traditional architectures — delivering the real-time computation speed, efficient historical backtesting, and streamlined development workflows necessary for rapid quantitative strategy evolution and deployment.

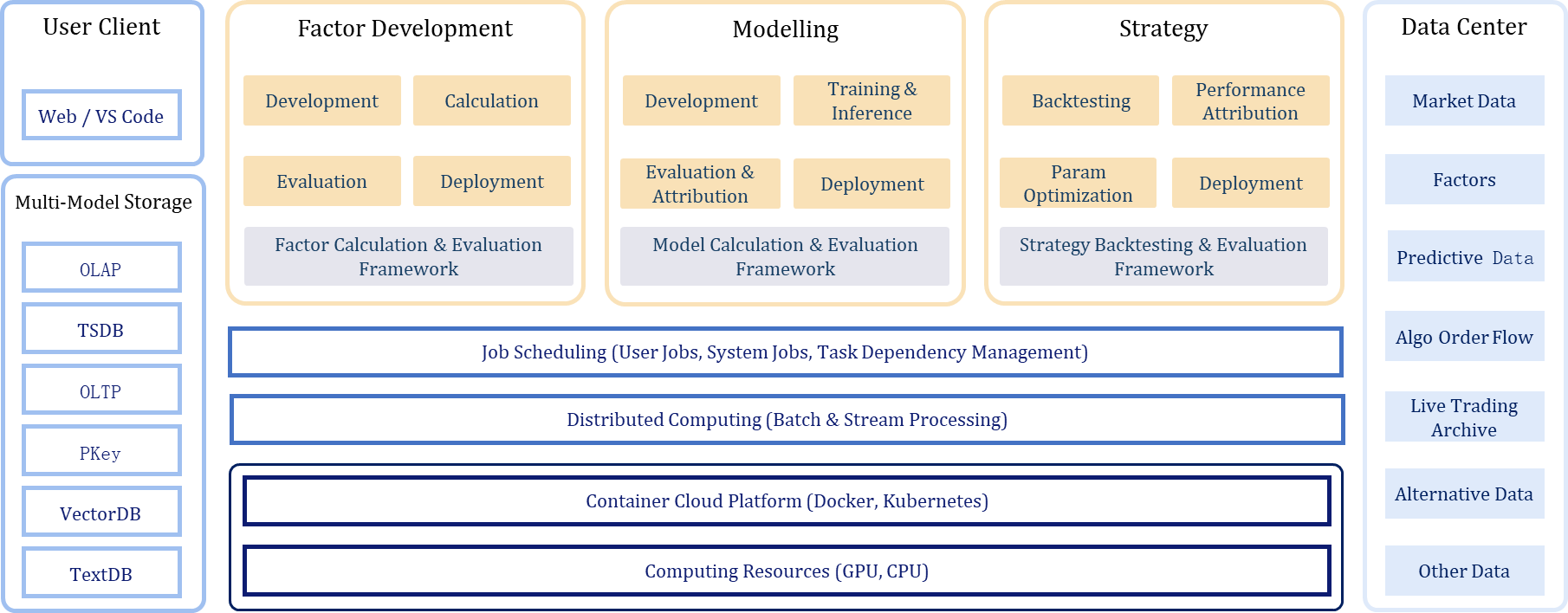

The DolphinDB Solution

To overcome these bottlenecks, DolphinDB enables hedge funds to build an integrated “research–backtest–production” factor development platform using its time-series database and unified batch and stream processing capabilities.

- Unified batch and stream processing

A single codebase handles both historical analysis and real-time calculations, eliminating the need for separate development tracks. Complex factor calculations complete within 5ms while processing over 1 million records per second. The platform includes more than 2,000 built-in functions covering statistics, time-series analysis, and machine learning applications.

- High-performance historical backtesting

The integrated backtesting engine leverages JIT optimizations to deliver 100× performance improvements over traditional approaches. Parallel computation capabilities support thousands of simultaneous factor tests while reducing resource consumption by approximately 80%. Event-driven backtesting, multi-factor analytics, and performance attribution tools come standard.

- Multi-model storage engines

An integrated storage architecture combines TSDB, OLAP, and OLTP capabilities to efficiently handle diverse financial data types. The system can query billions of factor data points in milliseconds while providing a unified query language and distributed framework that significantly reduces operational complexity.

- Production-grade factor development

Factor calculations are exposed as enterprise-ready services through C++, Java, and Python APIs. Real-time factor values stream directly to trading and risk management systems, while elastic scaling ensures stable operations during peak trading volumes and market volatility.

The Gains: Multi-Dimensional Breakthroughs

The deployment of DolphinDB’s solution has delivered significant, measurable improvements across multiple performance dimensions for leading hedge funds:

| Metric | Legacy System | DolphinDB | Speedup |

|---|---|---|---|

| Factor calc latency | 50–100 ms | ≤5 ms | 10–20× |

| Full-market backtest | 8 hours | ≤5 minutes | 100× |

| New factor deployment | 1 month | 1 week | 75% faster |

This solution's widespread adoption across multiple hedge funds validates three fundamental shifts in quantitative finance.

- Unified batch-stream architecture has become the new standard , enabling true "develop once, run anywhere" workflows that let researchers focus on factor innovation rather than technical implementation.

- Factor-as-a-Service is reshaping strategy development , transforming factor calculations into reusable digital assets that can be efficiently combined across different trading approaches.

- Real-time intelligence now defines competitive advantage. With millisecond-level factor calculations, hedge funds can finally execute genuinely data-driven, real-time trading decisions in increasingly competitive markets.