Case Study | How DolphinDB Optimizes End-to-End Market-Making for Financial Institutions

Market making is a vital function for maintaining market liquidity and has become a strategic focus for securities firms transforming their proprietary trading operations. As market-making activities expand and competition intensifies, institutions are under growing pressure to enhance capital efficiency, pricing precision, regulatory compliance, and real-time risk management.

Modern market-making systems must therefore satisfy two critical requirements:

- End-to-end integration that supports multi-market, multi-asset, and multifunctional workflows.

- Ultra-low latency and high agility , enabling millisecond-level responsiveness across the entire trading chain and rapid strategy iteration.

The Challenge: Overcoming High-Frequency Performance Bottlenecks

Through extensive collaboration with clients, DolphinDB has identified several recurring challenges that traditional database systems face in market-making environments:

- Insufficient market data granularity: Pricing models rely on high-frequency order book dynamics, yet second-level snapshots fail to capture transient market movements and microstructure fluctuations.

- Lagging metric computation: Limited real-time stream processing capabilities lead to delayed risk exposure monitoring, making it difficult to track positions and quotes with the required immediacy.

- Inefficient strategy development: Manually building simulation environments and rule engines is resource-intensive and time-consuming. Traditional backtesting frameworks also lack real-time margin and risk control mechanisms, making it challenging to replicate dynamic margin requirements and realistic trading conditions.

The DolphinDB Solution: Full-Chain Millisecond Responsiveness

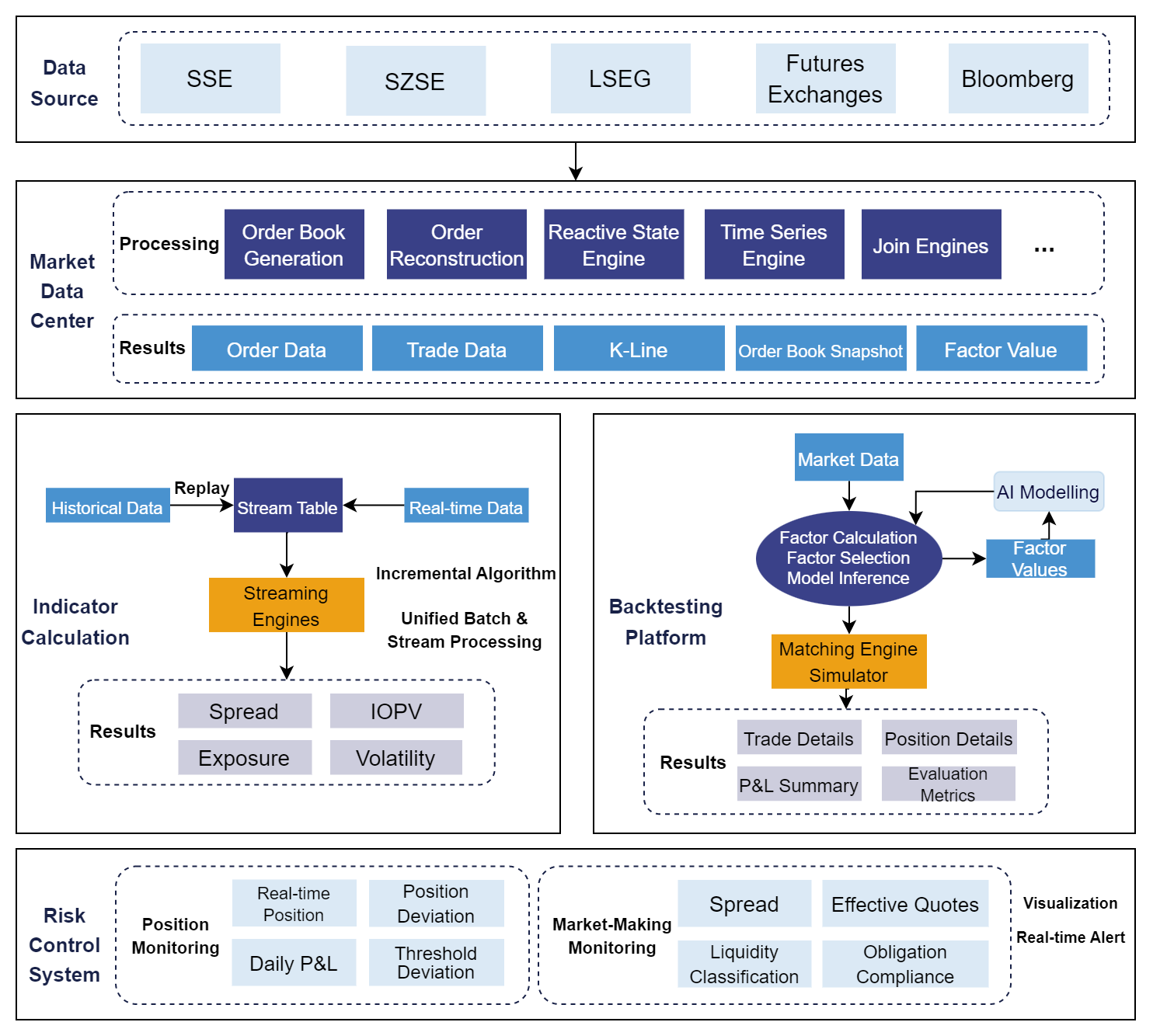

To address key market-making requirements—strategy development, data processing, order book generation, real-time quoting, and risk monitoring—DolphinDB leverages its self-developed streaming engine and backtesting plugin to achieve millisecond-level responsiveness across the entire workflow.

The DolphinDB solution covers market data processing, indicator computation, and strategy development, offering a unified, high-performance framework for market-making operations.

- Market Data Center : Supports tick-level data storage and analysis with dedicated computing engines and functions optimized for diverse market-making instruments, including equities, ETFs, bonds, futures, and options.

- Backtesting Platform : Features built-in backtesting and matching engine simulator that replicate all stages of mid- to high-frequency strategy testing, enabling precise order matching across multiple data sources.

- Risk Management System : Provides real-time metric computation through a unified framework that supports both streaming and batch risk indicators. Interactive dashboards deliver millisecond-level responsiveness from data ingestion to alert generation.

The Gains

With DolphinDB, securities firms have achieved end-to-end breakthroughs across data storage, market data processing, strategy development, and real-time risk management.

| Dimension | Legacy System | DolphinDB | Optimization |

|---|---|---|---|

| Historical Data Query | > 1 minute | ≤ 1 second | > 60× faster |

| Strategy Deployment Cycle | 3 months | 2 weeks | 85% shorter |

| Order Book Generation | Seconds-level or unavailable | ≤ 600 ns | Nanosecond-level performance for high-frequency trading |

| IOPV Computation | Batch-based, low real-time performance | < 1 ms | Real-time updates for enhanced pricing |

| Real-Time Risk Management | Second-level delay | < 1 ms | Instant alerts and monitoring |

By leveraging DolphinDB’s integrated development framework and high-performance streaming engines, financial institutions have broken through the performance barriers of traditional systems. It has reengineered market data processing, dramatically shortened strategy deployment cycles, and significantly strengthened real-time risk management capabilities.

Looking ahead, DolphinDB will continue to advance its product ecosystem—enhancing core components such as the curve fitting and pricing engines—to fully meet the evolving needs of securities firms and drive continuous innovation in the financial industry.