Turn Research into Revenue: Next-Gen Quant Platforms for Securities Firms

As financial institutions accelerate their digital transformation, the securities industry faces unprecedented operational demands. Growing asset class coverage, accelerating trading velocities, and increasing strategy complexity have exposed the limitations of traditional investment platforms—which struggle to deliver millisecond-level responsiveness and end-to-end integrated analytics.

DolphinDB addresses these challenges through a distributed architecture that unifies high-performance computation with stream-batch processing. Multiple securities firms have deployed DolphinDB to build integrated platforms spanning research, execution, and performance evaluation—breaking through traditional constraints in throughput, latency, and scalability. This shift is transforming quantitative investing from experience-based decision-making to data-driven intelligence.

The Challenge

Across brokerage engagements, DolphinDB sees five recurring pain points in modern investment decision platforms.

Data Fragmentation & Inconsistent Standards

Market data, reference information, and risk metrics are scattered across relational databases, NoSQL systems, and time-series stores—each with different data definitions and schemas. This fragmentation creates high integration costs, data quality issues, and limited cross-team trust in analytical outputs.

Performance Constraints & Tool Limitations

Python and MATLAB lack native distributed computing capabilities, forcing organizations to separate computation from storage. Heavy cross-system I/O overhead undermines high-frequency strategy development and real-time analytics, creating bottlenecks that limit research velocity.

Isolated Business Systems

Research, trading, and risk management operate in separate environments with manual data handoffs between teams. This isolation slows collaboration, increases operational overhead, and creates reconciliation challenges that impact decision quality.

Research-to-Production Friction

Dual codebases—typically Python for research and C++/Java for production—require complete strategy reimplementation before deployment. This doubles maintenance burden, extends time-to-market, and introduces reproducibility risks that can invalidate backtesting results.

Vendor Dependency & Limited Control

Proprietary platforms and reliance on foreign database systems create cost pressures, slow feature iteration, and introduce technology supply chain vulnerabilities that limit strategic flexibility and competitive differentiation.

The DolphinDB Solution

DolphinDB delivers an enterprise-grade, unified platform that addresses the fundamental limitations of traditional investment systems. By integrating real-time and historical analytics across the complete data lifecycle, it supports the end-to-end quantitative workflow—from research and backtesting through live execution and performance evaluation.

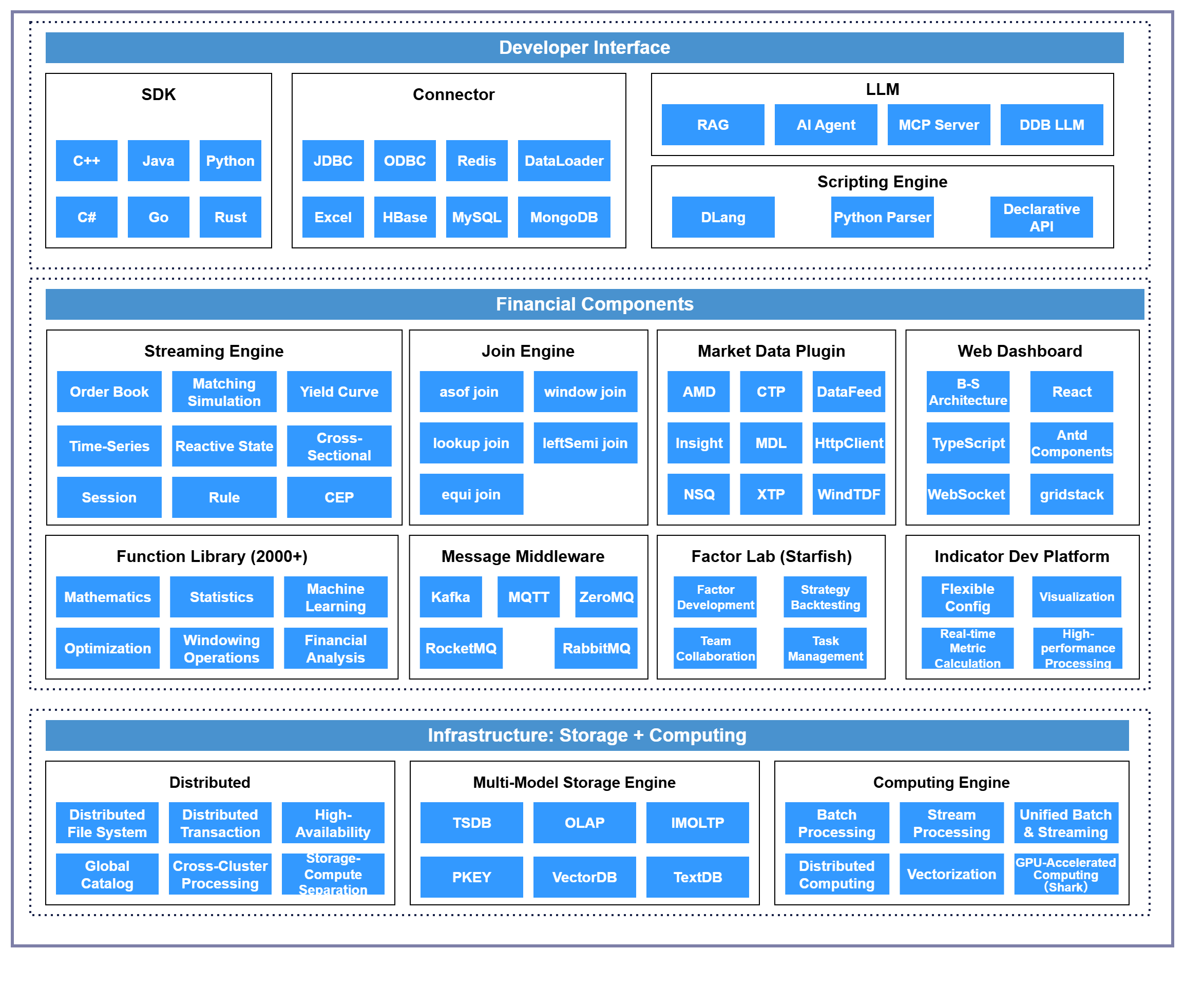

Technology Architecture

- DolphinDB's distributed database architecture provides the system backbone, featuring disaggregated storage and compute for high availability and elastic scalability. This foundation ensures consistent, low-latency data access across all upstream applications while maintaining enterprise-grade reliability.

- The platform incorporates 20+ specialized streaming engines purpose-built for financial workflows—including order book reconstruction, simulation matching, real-time factor calculation, and signal generation engines. These components handle complex event processing and stateful computations natively, eliminating the need for custom middleware or external frameworks.

- With over 2,000 built-in functions optimized for financial analytics—covering technical indicators, risk metrics, portfolio analytics, and time-series operations—the platform provides native support for quantitative research and production trading workflows. This integrated library accelerates development while ensuring consistency between research and execution environments.

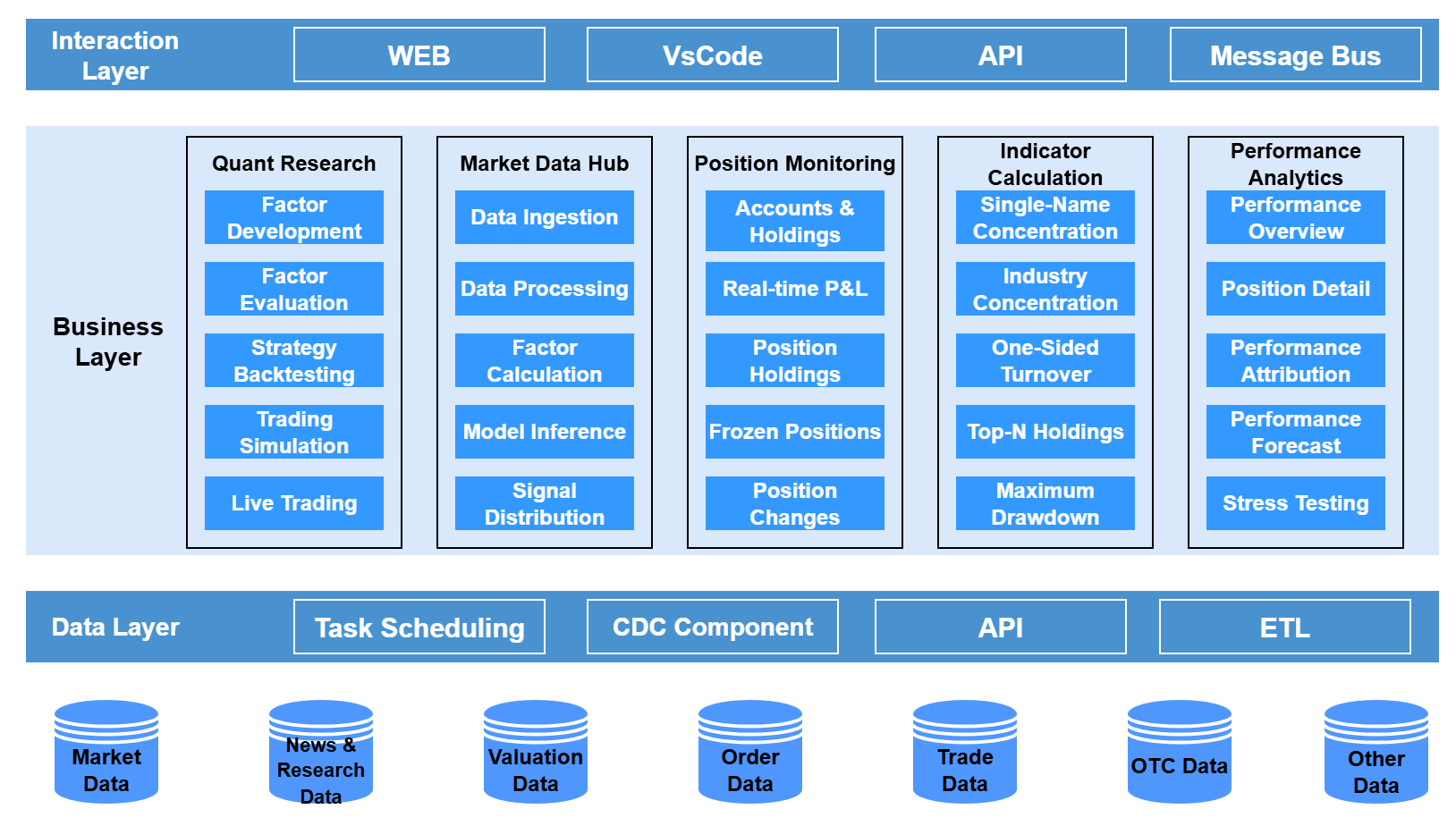

Business Architecture

Data Layer Orchestrates ingestion from multiple data sources through automated scheduling and change data capture (CDC) pipelines. Ensures downstream applications receive standardized, timely, and quality-controlled datasets with consistent schemas and lineage tracking.

Business Layer Supports core quantitative workflows across research, market data management, and portfolio monitoring. Provides specialized capabilities for factor engineering, alpha signal generation, real-time indicator calculation, pre-trade risk checks, compliance controls, and performance attribution—enabling end-to-end strategy lifecycle management.

Interaction Layer Offers flexible access through multiple interfaces: web-based consoles for monitoring and operations, VS Code integration for development workflows, and comprehensive APIs/SDKs for programmatic access. This multi-channel approach accommodates different user personas—from researchers and traders to system integrators and data engineers.

Application Scenarios

Unified Research Data Center Consolidates multi-source datasets into a centralized repository, eliminating data silos and providing consistent, governed data for quantitative analytics.

High-Performance Factor Engineering Distributed architecture with Raft consensus enables efficient batch computation and sub-millisecond real-time factor calculation using unified code—seamless promotion from research to production.

Integrated Backtesting & Simulation Native backtes engine and matching engine simulator support medium- to high-frequency strategy development. Includes performance attribution (Brinson, Campisi) to diagnose alpha sources.

Real-Time Risk Monitoring Millisecond-level risk metric computation with live exposure monitoring, pre-trade controls, and threshold-based alerting through visualization dashboards.

The Gains

| Scenario | Test Item | DolphinDB | Improvement |

|---|---|---|---|

| Trading Simulation | Simulated matching on 2,611 symbols / 1.3B ticks | 43s | Built-in matching engine simulator for HFT workloads |

| Trading Simulation | Simulated matching on 2,611 symbols / 1.3B ticks | 33s | Built-in matching engine simulator for HFT workloads |

| Strategy Backtesting | Equities: Snapshot-based intraday strategy | 1.1s | Built-in backtest plugin; >10× faster vs. Python |

| Strategy Backtesting | ETFs: Grid trading strategy | 2.1s | Built-in backtest plugin; >10× faster vs. Python |

| Strategy Backtesting | Futures: Continuous front-month (“main”) contract, on minute-bar data | 0.2s | Built-in backtest plugin; >10× faster vs. Python |

| CPU–GPU Hybrid Computing Platform | Snowball option pricing | ≤30ms | 20–100× |

| CPU–GPU Hybrid Computing Platform | Multi-dimensional Monte Carlo | 20ms | >100× |

| Factor Calculation | WorldQuant-1 factor on 1 year daily data | 86ms | >100× |

| Storage & Query | Write 200 factors on 3-sec bars, single symbol/day | 500ms | — |

| Storage & Query | Query 200 factors on 3-sec bars, single symbol/day | 50ms | — |

| Performance Attribution | Brinson (10 holdings × 10 years, daily) | 4,026ms | Built-in Brinson model → seconds-level |

| Performance Attribution | Campisi (10 holdings × 10 years, daily) | 358ms | Built-in Campisi model → milliseconds-level |

Deployment of the DolphinDB platform has delivered measurable value across securities operations. It establishes unified data governance —ensuring consistency across research, trading, and performance evaluation. The integrated architecture accelerates research-to-production workflows : by combining data management, stream-batch processing, and the native DolphinDB scripting language, firms reduce strategy deployment time by multiples. The platform also consolidates investment workflows end-to-end —from market analysis and execution through risk monitoring—eliminating system fragmentation and significantly improving operational efficiency.

In competitive capital markets, DolphinDB enables securities firms to build data-driven capabilities that break down organizational and technical silos—advancing quantitative operations toward greater intelligence, real-time responsiveness, and strategic agility.