Building Real-Time Order Book Snapshots at Any Frequency with DolphinDB

If you've ever tried to reconstruct a live order book from raw tick data, you know the pain. Latency spikes. Out-of-order messages. Memory pressure from thousands of instruments ticking simultaneously. Getting it right in production is non-trivial.

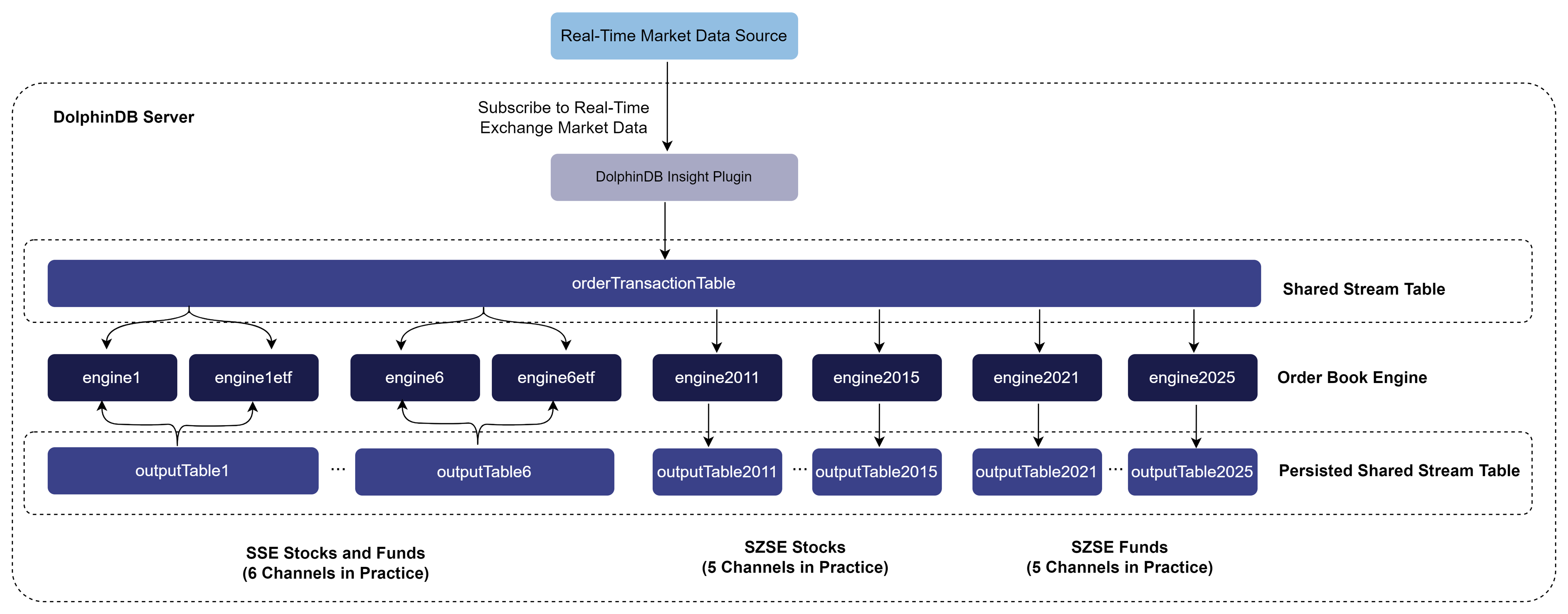

This post walks through a complete, production-oriented solution using DolphinDB together with the INSIGHT market data plugin to generate 1-second order book snapshots across all SSE and SZSE stocks and funds in real time. We'll cover everything from plugin installation to post-market batch writes to a distributed database — with the actual scripts you'd run in production.

What We're Building

The end-to-end pipeline looks like this:

- INSIGHT plugin receives tick-by-tick trade and order data from the exchange

- Data is written into per-channel stream tables in DolphinDB

- Order book engines subscribe to those stream tables and reconstruct the order book

- Snapshots are output to persisted stream tables at 1-second intervals

- After market close, all intraday data is batch-written to a DFS database

The solution handles 14 market data channels in total:

- Shanghai Stock Exchange (SSE) stocks & funds: channels 1–6

- Shenzhen Stock Exchange (SZSE) stocks: channels 2011–2015

- SZSE funds: channels 2021–2025

Prerequisites: DolphinDB Server 2.00.12+, a commercial license with the order book engine feature, and valid INSIGHT account credentials. The INSIGHT plugin runs on Linux only.

Step 1: Install and Load the INSIGHT Plugin

After starting your DolphinDB node, connect via the GUI, VS Code, or Web UI and run:

login("admin", "123456")

installPlugin("insight")This downloads the plugin binary and description file (PluginInsight.txt). Then load it:

loadPlugin("insight")A successful load returns a list of all functions the plugin exposes. Note that you can only load the plugin once per node session. To prevent errors when re-running scripts, wrap it in a try-catch:

try{ loadPlugin("Insight") }catch(ex){print ex}Step 2: Clean Up Any Existing State

Stream tables, engines, and subscriptions with duplicate names will throw errors. Before running (or re-running) the setup script, clean up the environment:

def cleanEnvironment(){

try {

tcpClient = insight::getHandle()

insight::unsubscribe(tcpClient)

insight::close(tcpClient)

} catch(ex) { print(ex) }

for(channelno_ in 1..6){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_) + "etf") } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_) + "etf") } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

for(channelno_ in 2011..2015){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

for(channelno_ in 2021..2025){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

undef all

}

cleanEnvironment()Step 3: Create the Stream Tables

Input Tables (Raw Tick Data)

The order book engine expects both trade and order data in a single combined table. The INSIGHT plugin merges them for you. First, get the schema:

orderTransactionSchema = insight::getSchema(`OrderTransaction)Then create one stream table per channel. The capacity parameter controls pre-allocated memory — tune it based on your tick volume and available RAM:

capacity = 10000000

colName = orderTransactionSchema[`name]

colType = orderTransactionSchema[`type]

//SSE stocks and funds

for(channelno_ in 1..6){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}

//SZSE stocks

for(channelno_ in 2011..2015){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}

// SZSE funds

for(channelno_ in 2021..2025){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}Output Tables (Order Book Snapshots)

Because the snapshot schema has ~80 columns, we use persisted stream tables to reduce memory pressure. Each output table covers one channel:

// Create a persisted stream table

cacheSize = 10000000

preCache = 0

depth = 10

suffix = string(1..depth)

colNames = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colTypes = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

cacheSize=5000000

preCache=0

for(channelno_ in 1..6){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}

for(channelno_ in 2011..2015){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}

for(channelno_ in 2021..2025){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}Make sure persistenceDir is set in your dolphindb.cfg (standalone) or cluster.cfg (cluster) before starting the node, or enableTableShareAndPersistence will fail.

Step 4: Create the Order Book Engines

One engine per channel — don't mix channels into a single engine instance, or your order book correctness will be compromised.

// Create order book engines

// Map the input table column names to the variables required by the order book engine for internal calculation

inputColMap = dict(`codeColumn`timeColumn`typeColumn`priceColumn`qtyColumn`buyOrderColumn`sellOrderColumn`sideColumn`msgTypeColumn`seqColumn, `SecurityID`MDTime`Type`Price`Qty`BuyNo`SellNo`BSFlag`SourceType`ApplSeqNum)

// Create a dictionary to define the previous day's closing prices, which will be passed to the prevClose parameter. prevClose does not affect any output columns other than the previous day's closing prices.

prevClose = dict(SYMBOL, DOUBLE)

// Define the engine to calculate and output 10-level bid and ask order books every 1 second

for(channelno_ in 1..6){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHG", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_) + "etf", exchange="XSHGFUND", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}

for(channelno_ in 2011..2015){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHE", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}

for(channelno_ in 2021..2025){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHEFUND", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}A few parameters worth highlighting:

- intervalInMilli=1000 — snapshot frequency in milliseconds. Change to 500 for 500ms snapshots; no schema changes needed.

- orderbookDepth=10 — number of bid/ask price levels. If you change this, update the output table schema's depth variable to match.

- orderBySeq=true — required because INSIGHT's TCP interface doesn't guarantee in-channel ordering. Set to false only if your data source delivers pre-sorted data.

- prevClose — pass in a pre-populated dict from historical data in production; the empty dict here is fine for testing.

Want derived metrics or custom factors?

The engine supports outputColMap (to select specific output fields) and userDefinedMetrics (to compute custom factors within each snapshot window). For example, you can output average order duration and cancellation volume alongside the order book:

def userDefinedFunc(t){

AvgBuyDuration = rowAvg(t.TradeMDTimeList - t.TradeOrderBuyNoTimeList).int()

AvgSellDuration = rowAvg(t.TradeMDTimeList - t.TradeOrderSellNoTimeList).int()

BuyWithdrawQty = rowSum(t.WithdrawBuyQtyList)

SellWithdrawQty = rowSum(t.WithdrawSellQtyList)

return (AvgBuyDuration, AvgSellDuration, BuyWithdrawQty, SellWithdrawQty)

}Pass it to the engine via userDefinedMetrics=userDefinedFunc. When you do, remember to extend the output table schema with the corresponding columns.

Step 5: Wire the Stream Tables to the Engines

Subscribe each input stream table to its corresponding engine. The hash parameter distributes subscription processing across background worker threads:

subscribeTable(tableName="orderTransactionTable1", actionName="orderbookDemo1", handler=getStreamEngine("orderbookEngine1"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=0)

subscribeTable(tableName="orderTransactionTable2", actionName="orderbookDemo2", handler=getStreamEngine("orderbookEngine2"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=1)

// ... repeat for channels 3–6

subscribeTable(tableName="orderTransactionTable1", actionName="orderbookDemo1etf", handler=getStreamEngine("orderbookEngine1etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=0)

// ... repeat ETF subscriptions for channels 2–6

subscribeTable(tableName="orderTransactionTable2011", actionName="orderbookDemo2011", handler=getStreamEngine("orderbookEngine2011"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=6)

// ... repeat for 2012–2015 and 2021–2025batchSize=1 and throttle=0.001 together mean data is forwarded to the engine almost immediately on arrival. Spread channels across different hash values to keep CPU load balanced.

Step 6: Connect to INSIGHT and Start the Feed

HOST = "your.insight.host"

PORT = 1234

USER = "your_user"

PASSWORD = "your_password"

handles = dict(

['OrderTransaction'],

[dict(

[1,2,3,4,5,6,2011,2012,2013,2014,2015,2021,2022,2023,2024,2025],

[orderTransactionTable1, orderTransactionTable2, orderTransactionTable3,

orderTransactionTable4, orderTransactionTable5, orderTransactionTable6,

orderTransactionTable2011, orderTransactionTable2012, orderTransactionTable2013,

orderTransactionTable2014, orderTransactionTable2015, orderTransactionTable2021,

orderTransactionTable2022, orderTransactionTable2023, orderTransactionTable2024,

orderTransactionTable2025]

)]

)

tcpClient = insight::connect(handles, HOST, PORT, USER, PASSWORD,,,true)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHE, `StockType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHG, `StockType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHG, `FundType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHE, `FundType)At this point, tick data flows in, the engines reconstruct order books, and snapshots land in the output tables — all in real time.

To check ingestion status at any time:

tcpClient = insight::getHandle()

insight::getStatus(tcpClient)Step 7: Batch-Write Intraday Data to a DFS Database

When compute resources are tight, you can skip real-time database writes and instead batch everything to disk after market close. First, set up the databases and tables:

if(!existsDatabase("dfs://SZ_TB")) {

// Create a DFS database

dbDate = database(, partitionType=VALUE, partitionScheme=2023.01.01..2024.01.01)

dbID = database(, partitionType=HASH, partitionScheme=[SYMBOL, 25])

db = database(directory="dfs://SZ_TB", partitionType=COMPO, partitionScheme=[dbDate, dbID],engine='TSDB',atomic='CHUNK')

}

if(!existsDatabase("dfs://SH_TB")) {

// Create a DFS database

dbDate = database(, partitionType=VALUE, partitionScheme=2023.01.01..2024.01.01)

dbID = database(, partitionType=HASH, partitionScheme=[SYMBOL, 25])

db = database(directory="dfs://SH_TB", partitionType=COMPO, partitionScheme=[dbDate, dbID],engine='TSDB',atomic='CHUNK')

}

if(!existsTable("dfs://SZ_TB", "orderTransactionTable")) {

db = database("dfs://SZ_TB")

// Create a DFS table to store market data

colName = `SecurityID`MDDate`MDTime`SecurityIDSource`SecurityType`Index`SourceType`Type`Price`Qty`BSFlag`BuyNo`SellNo`ApplSeqNum`ChannelNo`receivedTime

colType = [SYMBOL,DATE,TIME,SYMBOL,SYMBOL,LONG,INT,INT,LONG,LONG,INT,LONG,LONG,LONG,INT,NANOTIMESTAMP]

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="orderTransactionTable",partitionColumns=`MDDate`SecurityID,sortColumns=`SecurityID`MDTime)

}

if(!existsTable("dfs://SH_TB", "orderTransactionTable")) {

db = database("dfs://SH_TB")

// Create a DFS table to store market data

colName = `SecurityID`MDDate`MDTime`SecurityIDSource`SecurityType`Index`SourceType`Type`Price`Qty`BSFlag`BuyNo`SellNo`ApplSeqNum`ChannelNo`receivedTime

colType = [SYMBOL,DATE,TIME,SYMBOL,SYMBOL,LONG,INT,INT,LONG,LONG,INT,LONG,LONG,LONG,INT,NANOTIMESTAMP]

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="orderTransactionTable",partitionColumns=`MDDate`SecurityID,sortColumns=`SecurityID`MDTime)

}

if(!existsTable("dfs://SZ_TB", "tick1sTable")) {

db = database("dfs://SZ_TB")

// Create a DFS table to store generated snapshot data

depth = 10

suffix = string(1..depth)

colName = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colType = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="tick1sTable",partitionColumns=`timestamp`SecurityID,sortColumns=`SecurityID`timestamp)

}

if(!existsTable("dfs://SH_TB", "tick1sTable")) {

db = database("dfs://SH_TB")

// Create a DFS table to store generated snapshot data

depth = 10

suffix = string(1..depth)

colName = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colType = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="tick1sTable",partitionColumns=`timestamp`SecurityID,sortColumns=`SecurityID`timestamp)

}Then write tick data directly from the in-memory stream tables, and subscribe snapshot tables with offset=0 to write from the beginning:

SH_orderTransaction = loadTable("dfs://SH_TB", "orderTransactionTable")

SZ_orderTransaction = loadTable("dfs://SZ_TB", "orderTransactionTable")

SH_output = loadTable("dfs://SH_TB", "tick1sTable")

SZ_output = loadTable("dfs://SZ_TB", "tick1sTable")

for(channelno_ in 1..6){

SH_orderTransaction.append!(objByName(`orderTransactionTable + string(channelno_)))

}

for(channelno_ in 2011..2025){

SZ_orderTransaction.append!(objByName(`orderTransactionTable + string(channelno_)))

}

for(channelno_ in 1..6){

subscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_), offset=0, handler=tableInsert{SH_output}, msgAsTable=true, batchSize=20000, throttle=5, reconnect=true, hash=13)

}

for(channelno_ in 2011..2025){

subscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_), offset=0, handler=tableInsert{SZ_output}, msgAsTable=true, batchSize=20000, throttle=5, reconnect=true, hash=14)

}The script then polls until all rows have landed in the DFS tables before declaring success.

Auto-Start at Node Startup

To make the whole pipeline start automatically when DolphinDB restarts, add the full setup script to a startup.dos file in your server directory, then configure in dolphindb.cfg (standalone) or cluster.cfg (cluster):

startup=/DolphinDB/server/startup.dosWhen the log shows Start orderbook service successfully!, everything is live. The cleanup function at the top of the script ensures idempotent restarts.

Key Takeaways

Building a production-grade real-time order book isn't just about the reconstruction algorithm — it's about the full data pipeline: ingestion, routing by channel, engine isolation, memory management for wide output schemas, and reliable post-market persistence. DolphinDB's combination of stream tables, subscription-based fanout, and the order book engine handles all of this with relatively concise script code.

A few things to keep in mind as you adapt this for your own environment:

- Tune capacity and cacheSize based on your actual tick volume. Under-provisioning these leads to unnecessary latency spikes.

- One engine per channel is non-negotiable for correctness.

- orderBySeq=true is the safe default for TCP-based feeds; disable it only when you're certain your source delivers ordered data.

- The intervalInMilli and orderbookDepth parameters give you flexible control over output granularity — changing the frequency requires no schema changes, but changing the depth does.

The same pattern generalizes cleanly to other DolphinDB market data plugins (amdQuote, MDL, NSQ) — only the INSIGHT-specific subscription calls need to change.

Appendix

- For detailed information on startup script configuration, refer to the documentation Startup Scripts.

- Real-time order book generation script (requires user-specific INSIGHT credentials)

login("admin", "123456")

try{ loadPlugin("insight") }catch(ex){print ex}

go

def cleanEnvironment(){

try {

tcpClient = insight::getHandle()

insight::unsubscribe(tcpClient)

insight::close(tcpClient)

} catch(ex) { print(ex) }

for(channelno_ in 1..6){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_) + "etf") } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_) + "etf") } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

for(channelno_ in 2011..2015){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

for(channelno_ in 2021..2025){

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderbookDemo" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="orderTransactionTable" + string(channelno_), actionName="orderTransactionTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { unsubscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamEngine("orderbookEngine" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("orderTransactionTable" + string(channelno_)) } catch(ex) { print(ex) }

try { dropStreamTable("outputTable" + string(channelno_)) } catch(ex) { print(ex) }

}

undef all

}

cleanEnvironment()

go

// Create stream tables for INSIGHT market data ingestion

orderTransactionSchema = insight::getSchema(`OrderTransaction);

capacity = 10000000

colName = orderTransactionSchema[`name]

colType = orderTransactionSchema[`type]

//SSE stocks and funds

for(channelno_ in 1..6){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}

//SZSE stocks

for(channelno_ in 2011..2015){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}

// SZSE funds

for(channelno_ in 2021..2025){

share(streamTable(capacity:0, colName, colType), `orderTransactionTable + string(channelno_))

}

// Create a persisted stream table

cacheSize = 10000000

preCache = 0

depth = 10

suffix = string(1..depth)

colNames = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colTypes = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

cacheSize=5000000

preCache=0

for(channelno_ in 1..6){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}

for(channelno_ in 2011..2015){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}

for(channelno_ in 2021..2025){

enableTableShareAndPersistence(table=streamTable(cacheSize:0, colNames, colTypes), tableName=`outputTable + string(channelno_), cacheSize=cacheSize, preCache=preCache)

}

go

// Create an order book engine

// Map the input table column names to the variables required by the order book engine for internal calculation

inputColMap = dict(`codeColumn`timeColumn`typeColumn`priceColumn`qtyColumn`buyOrderColumn`sellOrderColumn`sideColumn`msgTypeColumn`seqColumn, `SecurityID`MDTime`Type`Price`Qty`BuyNo`SellNo`BSFlag`SourceType`ApplSeqNum)

// Create a dictionary to define the previous day's closing prices, which will be passed to the prevClose parameter. prevClose does not affect any output columns other than the previous day's closing prices.

prevClose = dict(SYMBOL, DOUBLE)

for(channelno_ in 1..6){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHG", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_) + "etf", exchange="XSHGFUND", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}

for(channelno_ in 2011..2015){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHE", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}

for(channelno_ in 2021..2025){

createOrderBookSnapshotEngine(name="orderbookEngine" + string(channelno_), exchange="XSHEFUND", orderbookDepth=10, intervalInMilli=1000, date=date(now()), startTime=09:30:00.000, prevClose=prevClose, dummyTable=objByName("orderTransactionTable" + string(channelno_)), inputColMap=inputColMap, outputTable=objByName("outputTable" + string(channelno_)), orderBySeq=true)

}

// Subscribe to the stream table, synthesize snapshots, and output them to the order book engine

subscribeTable(tableName="orderTransactionTable1", actionName="orderbookDemo1", handler=getStreamEngine("orderbookEngine1"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=0)

subscribeTable(tableName="orderTransactionTable2", actionName="orderbookDemo2", handler=getStreamEngine("orderbookEngine2"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=1)

subscribeTable(tableName="orderTransactionTable3", actionName="orderbookDemo3", handler=getStreamEngine("orderbookEngine3"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=2)

subscribeTable(tableName="orderTransactionTable4", actionName="orderbookDemo4", handler=getStreamEngine("orderbookEngine4"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=3)

subscribeTable(tableName="orderTransactionTable5", actionName="orderbookDemo5", handler=getStreamEngine("orderbookEngine5"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=4)

subscribeTable(tableName="orderTransactionTable6", actionName="orderbookDemo6", handler=getStreamEngine("orderbookEngine6"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=5)

subscribeTable(tableName="orderTransactionTable1", actionName="orderbookDemo1etf", handler=getStreamEngine("orderbookEngine1etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=0)

subscribeTable(tableName="orderTransactionTable2", actionName="orderbookDemo2etf", handler=getStreamEngine("orderbookEngine2etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=1)

subscribeTable(tableName="orderTransactionTable3", actionName="orderbookDemo3etf", handler=getStreamEngine("orderbookEngine3etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=2)

subscribeTable(tableName="orderTransactionTable4", actionName="orderbookDemo4etf", handler=getStreamEngine("orderbookEngine4etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=3)

subscribeTable(tableName="orderTransactionTable5", actionName="orderbookDemo5etf", handler=getStreamEngine("orderbookEngine5etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=4)

subscribeTable(tableName="orderTransactionTable6", actionName="orderbookDemo6etf", handler=getStreamEngine("orderbookEngine6etf"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=5)

subscribeTable(tableName="orderTransactionTable2011", actionName="orderbookDemo2011", handler=getStreamEngine("orderbookEngine2011"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=6)

subscribeTable(tableName="orderTransactionTable2012", actionName="orderbookDemo2012", handler=getStreamEngine("orderbookEngine2012"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=7)

subscribeTable(tableName="orderTransactionTable2013", actionName="orderbookDemo2013", handler=getStreamEngine("orderbookEngine2013"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=8)

subscribeTable(tableName="orderTransactionTable2014", actionName="orderbookDemo2014", handler=getStreamEngine("orderbookEngine2014"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=9)

subscribeTable(tableName="orderTransactionTable2015", actionName="orderbookDemo2015", handler=getStreamEngine("orderbookEngine2015"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=10)

subscribeTable(tableName="orderTransactionTable2021", actionName="orderbookDemo2021", handler=getStreamEngine("orderbookEngine2021"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=6)

subscribeTable(tableName="orderTransactionTable2022", actionName="orderbookDemo2022", handler=getStreamEngine("orderbookEngine2022"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=7)

subscribeTable(tableName="orderTransactionTable2023", actionName="orderbookDemo2023", handler=getStreamEngine("orderbookEngine2023"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=8)

subscribeTable(tableName="orderTransactionTable2024", actionName="orderbookDemo2024", handler=getStreamEngine("orderbookEngine2024"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=9)

subscribeTable(tableName="orderTransactionTable2025", actionName="orderbookDemo2025", handler=getStreamEngine("orderbookEngine2025"), msgAsTable=true, batchSize=1, throttle=0.001, reconnect=true, hash=10)

go

// Configure account information

HOST = "111.111.111.111"

PORT = 111

USER = "111"

PASSWORD = "111"

// Subscribe to INSIGHT market data: stocks and funds

handles = dict(['OrderTransaction'], [dict([1,2,3,4,5,6,2011,2012,2013,2014,2015,2021,2022,2023,2024,2025], [orderTransactionTable1,orderTransactionTable2,orderTransactionTable3,orderTransactionTable4,orderTransactionTable5,orderTransactionTable6,orderTransactionTable2011,orderTransactionTable2012,orderTransactionTable2013,orderTransactionTable2014,orderTransactionTable2015,orderTransactionTable2021,orderTransactionTable2022,orderTransactionTable2023,orderTransactionTable2024,orderTransactionTable2025])])

tcpClient= insight::connect(handles,HOST, PORT, USER, PASSWORD,,,true)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHE, `StockType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHG, `StockType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHG, `FundType)

insight::subscribe(tcpClient, [`MD_ORDER_TRANSACTION], `XSHE, `FundType)

writeLog("Start orderbook service successfully!")- Batch write intraday data into the DFS database

// Create a DFS table

if(!existsDatabase("dfs://SZ_TB")) {

// Create a DFS database

dbDate = database(, partitionType=VALUE, partitionScheme=2023.01.01..2025.01.01)

dbID = database(, partitionType=HASH, partitionScheme=[SYMBOL, 25])

db = database(directory="dfs://SZ_TB", partitionType=COMPO, partitionScheme=[dbDate, dbID],engine='TSDB',atomic='CHUNK')

}

if(!existsDatabase("dfs://SH_TB")) {

// Create a DFS database

dbDate = database(, partitionType=VALUE, partitionScheme=2023.01.01..2025.01.01)

dbID = database(, partitionType=HASH, partitionScheme=[SYMBOL, 25])

db = database(directory="dfs://SH_TB", partitionType=COMPO, partitionScheme=[dbDate, dbID],engine='TSDB',atomic='CHUNK')

}

if(!existsTable("dfs://SZ_TB", "orderTransactionTable")) {

db = database("dfs://SZ_TB")

// Create a DFS table to store market data

colName = `SecurityID`MDDate`MDTime`SecurityIDSource`SecurityType`Index`SourceType`Type`Price`Qty`BSFlag`BuyNo`SellNo`ApplSeqNum`ChannelNo`receivedTime

colType = [SYMBOL,DATE,TIME,SYMBOL,SYMBOL,LONG,INT,INT,LONG,LONG,INT,LONG,LONG,LONG,INT,NANOTIMESTAMP]

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="orderTransactionTable",partitionColumns=`MDDate`SecurityID,sortColumns=`SecurityID`MDTime)

}

if(!existsTable("dfs://SH_TB", "orderTransactionTable")) {

db = database("dfs://SH_TB")

// Create a DFS table to store market data

colName = `SecurityID`MDDate`MDTime`SecurityIDSource`SecurityType`Index`SourceType`Type`Price`Qty`BSFlag`BuyNo`SellNo`ApplSeqNum`ChannelNo`receivedTime

colType = [SYMBOL,DATE,TIME,SYMBOL,SYMBOL,LONG,INT,INT,LONG,LONG,INT,LONG,LONG,LONG,INT,NANOTIMESTAMP]

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="orderTransactionTable",partitionColumns=`MDDate`SecurityID,sortColumns=`SecurityID`MDTime)

}

if(!existsTable("dfs://SZ_TB", "tick1sTable")) {

db = database("dfs://SZ_TB")

// Create a DFS table to store generated snapshot data

depth = 10

suffix = string(1..depth)

colName = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colType = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="tick1sTable",partitionColumns=`timestamp`SecurityID,sortColumns=`SecurityID`timestamp)

}

if(!existsTable("dfs://SH_TB", "tick1sTable")) {

db = database("dfs://SH_TB")

// Create a DFS table to store generated snapshot data

depth = 10

suffix = string(1..depth)

colName = `SecurityID`timestamp`lastAppSeqNum`tradingPhaseCode`modified`turnover`volume`tradeNum`totalTurnover`totalVolume`totalTradeNum`lastPx`highPx`lowPx`ask`bid`askVol`bidVol`preClosePx`invalid join ("bids" + suffix) join ("bidVolumes" + suffix) join ("bidOrderNums" + suffix) join ("asks" + suffix) join ("askVolumes" + suffix) join ("askOrderNums" + suffix)

colType = [SYMBOL,TIMESTAMP,LONG,INT,BOOL,DOUBLE,LONG,INT,DOUBLE,LONG,INT,DOUBLE,DOUBLE,DOUBLE,DOUBLE,DOUBLE,LONG,LONG,DOUBLE,BOOL] join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth) join take(DOUBLE, depth) join take(LONG, depth) join take(INT, depth)

tbSchema = table(1:0, colName, colType)

db.createPartitionedTable(table=tbSchema,tableName="tick1sTable",partitionColumns=`timestamp`SecurityID,sortColumns=`SecurityID`timestamp)

}

// Store market data and snapshot data in the DFS database

SZ_orderTransaction = loadTable("dfs://SZ_TB", "orderTransactionTable")

SZ_output = loadTable("dfs://SZ_TB", "tick1sTable")

SH_orderTransaction = loadTable("dfs://SH_TB", "orderTransactionTable")

SH_output = loadTable("dfs://SH_TB", "tick1sTable")

for(channelno_ in 1..6){

SH_orderTransaction.append!(objByName(`orderTransactionTable + string(channelno_)))

}

for(channelno_ in 2011..2015){

SZ_orderTransaction.append!(objByName(`orderTransactionTable + string(channelno_)))

}

for(channelno_ in 2021..2025){

SZ_orderTransaction.append!(objByName(`orderTransactionTable + string(channelno_)))

}

for(channelno_ in 1..6){

subscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_), offset=0, handler=tableInsert{SH_output}, msgAsTable=true, batchSize=20000, throttle=5, reconnect=true, hash=13)

}

for(channelno_ in 2011..2015){

subscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_), offset=0, handler=tableInsert{SZ_output}, msgAsTable=true, batchSize=20000, throttle=5, reconnect=true, hash=14)

}

for(channelno_ in 2021..2025){

subscribeTable(tableName="outputTable" + string(channelno_), actionName="outputTableInsert" + string(channelno_), offset=0, handler=tableInsert{SZ_output}, msgAsTable=true, batchSize=20000, throttle=5, reconnect=true, hash=15)

}

SH_Count = exec count(*) from SH_output where date(timestamp) = date(now())

SZ_Count = exec count(*) from SZ_output where date(timestamp) = date(now())

SH_Total_Count = 0

SZ_Total_Count = 0

for(channelno_ in 1..6){

SH_Total_Count += getPersistenceMeta(objByName(`outputTable + string(channelno_)))[`totalSize]

}

for(channelno_ in 2011..2015){

SZ_Total_Count += getPersistenceMeta(objByName(`outputTable + string(channelno_)))[`totalSize]

}

for(channelno_ in 2021..2025){

SZ_Total_Count += getPersistenceMeta(objByName(`outputTable + string(channelno_)))[`totalSize]

}

do{

SH_Count = exec count(*) from SH_output where date(timestamp) = date(now())

SZ_Count = exec count(*) from SZ_output where date(timestamp) = date(now())

}while(SH_Count != SH_Total_Count || SZ_Count != SZ_Total_Count)

writeLog("All data has been written to the dfs database.")Thanks for reading! Stay connected with DolphinDB by following us on X (@DolphinDB_Inc) and LinkedIn for the latest updates, technical articles, and product news.